Day 33 – Q 5. Examine the implications of non-performing assets (NPAs) for India’s industrial sector.

5. Examine the implications of non-performing assets (NPAs) for India’s industrial sector.

भारत के औद्योगिक क्षेत्र के लिए गैर-निष्पादित संपत्ति (एनपीए) के प्रभावों की जांच करें।

Introduction

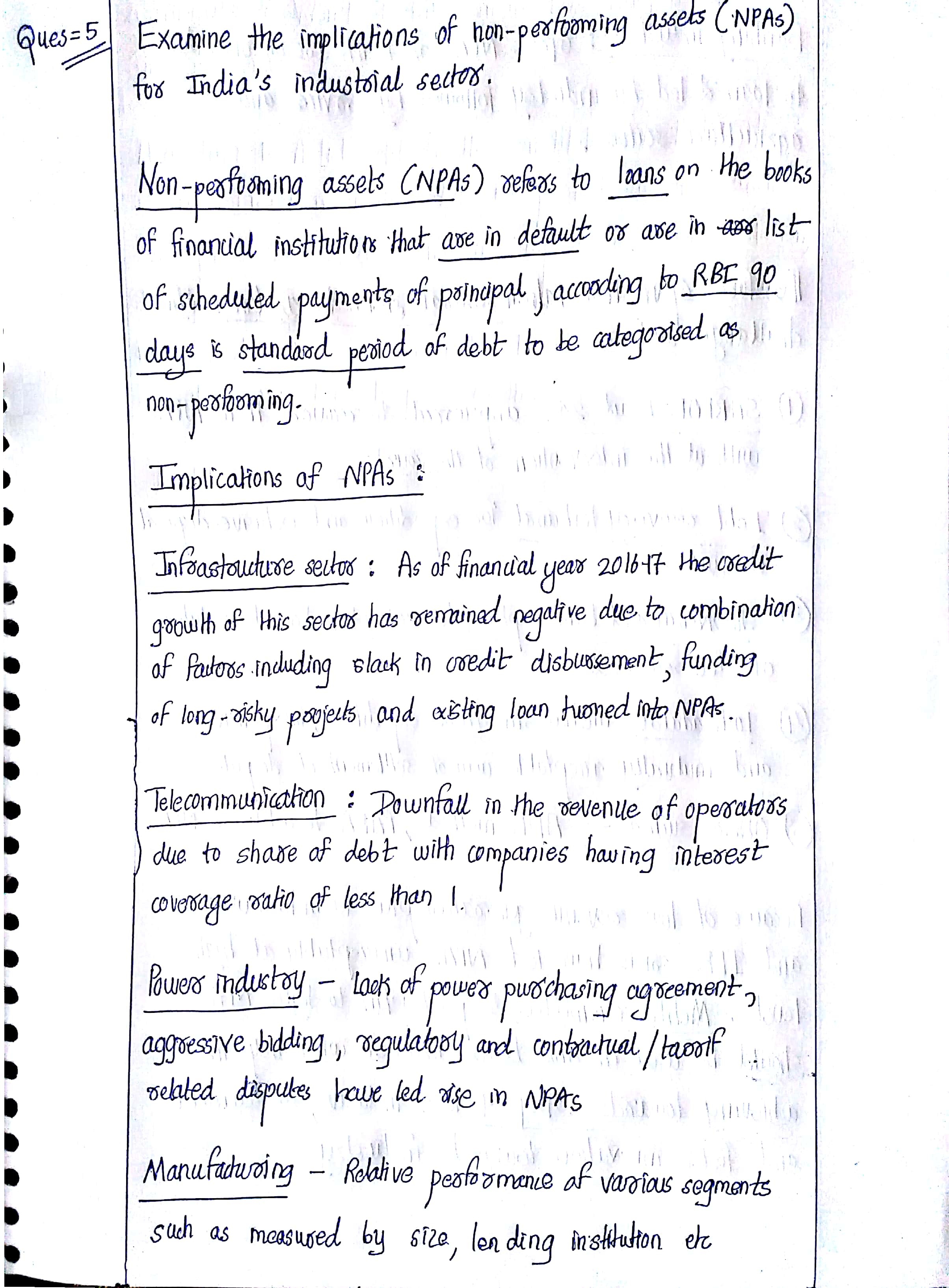

Non-performing assets (NPA) is a loan for which interest or principal is overdue for 90 days. Gross NPA ratio in India stands at 12%, which is one of worst among major economies of the world. This rising NPA has major impacts on some industries of the country:

Body

- POWER SECTOR: Power sector, especially one dependant on coal, has largely contributed to NPA in India. Low capacity utilization, difficulty in coal imports, land and environment clearances have led to debt ridden distribution companies. The government aim of 24×7 electricity supply, scaling up to cleaner fuel based electricity or to improve health of DISCOMs is halted due to credit constraint.

- Infrastructure Sector: Connectivity is the backbone of any country. With the surmounting loans and the non-availability of fresh credit along with liquidity crunch had put this on backtrack. Growing NPA in this sector have led to stalled projects, reluctance of private sector towards PPP projects.

- Real estate: A sector, which is second largest employment generator in India after agriculture, has seen decline in bank lending due to rising number of defaulting developers

- Telecommunication: politicisation of sector, Sudden boom had led to indiscriminate lending to the sector. Economic slowdown slowly piled up bad loans in the sector leading to reduced competition among telecom providers and decrease in service efficiency

- Financial SECTOR: Financial institutes were reluctant to lend having learnt the lesson, less capital available for investors and the institutes themselves had to bear with low profits

- Banking Sector: Banks works as oxygen for an economy. The deteriorating health of banking sector had undesirable spill over effect on all sectors.

- MSMEs: The MSMEs are the small establishment with periodic need of credit to continue their operation. The unavailability of loans forces them to shut down and hence leave large population unemployed.

Government over the period came up with a slew of measures to deal with NPA including legislative/executive/judicial reforms such as

- IBC 2016,

- Bank recapitalisation under Indradhanush.

- Increased oversight by RBI through amending banking regulation act and Prompt corrective action,

- Bad banks, bank mergers, ARC,

- FRDI bill, SARFAESI act,

- Capital infusion in PSBs worth 2.11 lakh crores ,

- SEBI guidelines to credit agencies after IL&FS failure,

- Recommendation of committees such as P J Nayak , Mehta committee etc.

Conclusion

If India aims to increase its growth rate to double figure, resolving NPA problem should be a preference. Sticking to healthy banking principles , more autonomy to banks coupled by effective oversight by RBI and reduced political interference is a way to go

Best answer DP

{kind=link}